- Client specific requirements and fund information in German remain biggest problems

- Regulation causes two-thirds of asset managers more work in Germany than in their home market

- ESMA rules: Less than a third want to change investment process or fund names for existing funds

- Home office: Nine out of ten employees are allowed to work more often from home

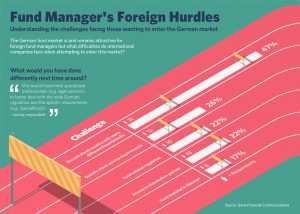

14 April 2025, South Petherton (UK) – Client specific requirements (27%), such as reporting or tax requirements, providing fund information in German language (22%) and the decentralised structure of Germany with its various financial centres (17%) are the biggest challenges for foreign investment companies in the German market. Access to distribution partners (14%), recruitment of qualified staff (10%) and fund related regulation (7%) are considered further hurdles.

Two-thirds (67%) of foreign fund houses feel that regulation in Germany is more labour-intensive overall than in their home market.

These are key findings of the annual online survey “The biggest challenges for foreign fund managers in the German market” conducted by Gerle Financial Communications, a specialised communications consultancy for the financial sector. Representatives of 30 foreign fund companies and external sales representatives (third-party marketers) took part in the survey in February and March 2025. It was the sixth survey since 2020.

The survey also reveals that six out of ten (62%) asset managers see no reason to change anything in their ESG funds if the European fund regulator Esma imposes stricter requirements on the names of existing funds from May onwards. Only 17% will change the names of the corresponding funds. 14% want to adapt their investment process to comply with the new regulations.

The most common weekly “working from home” model among representatives of foreign investment companies is “3 days at home / 2 days in the office” (44%). Overall, nine out of ten employees in the fund industry are allowed to work more days from home than in the office.

Almost half manage more than one billion euros for German customers

A look at the origin, market affiliation and size of the participating companies: Over two thirds are headquartered in Europe, i.e. the EU (38%), the UK (23%) and the EFTA states of Norway, Switzerland and Liechtenstein (8%). They are followed by companies from the US (18%), Canada (8%), Chile and South Africa (3% each).[1]

Two thirds of the participants (67%) came to Germany more than ten years ago; a quarter (23%) have been active in Germany for between five and ten years and the remaining 10% for between three and five years.

On behalf of German clients, almost half (48%) of the foreign asset managers represented administer assets of more than one billion euros: according to the survey, 17% have more than ten billion, 14% between five and ten billion and a further 17% between one and five billion euros under their management. Below the one-billion-euro threshold in assets under management, the breakdown is as follows: 500 million to one billion euros (17%), 100 to 500 million euros (21%) and less than 100 million euros (7%). 7% of respondents did not wish to disclose any information on their assets.

Client specific requirements and German fund material are the biggest hurdles

The biggest challenge for foreign fund companies in Germany are client specific requirements (27%), e.g. in the areas of reporting and taxes. This is a higher proportion than last year (25%). One in five participants (22%) consider it difficult to provide fund-related information material in German – in 2024, 18% said the same. The fact that Germany’s decentralised structure with its various financial centres represents a hurdle was cited by 17% (2024: 19%).

Only 14% (2024: 18%) still consider gaining access to sales partners to be a challenge. Recruiting qualified staff is a problem for one in ten respondents (10%), compared to 7% last year. The regulation of funds in Germany is seen as less of an obstacle at 7% compared to the previous year (9%). “Other challenges” came in at 3% (2024: 5%).

Regulation in Germany is more work than in domestic markets

However, overall 67% of participants stated this year that regulation in Germany caused them more work compared to their home market – the remaining third considered the workload to be “just as high”.

Another labour-intensive issue evidently is the process of monitoring, selecting and managing sustainable and socially responsible investments (ESG/SRI): 39% of respondents (2024: 37%) stated that this was more laborious in Germany than in their home country. As in the previous year (56%), more than half (57%) have just as much work with ESG/SRI in Germany as at home.

When it comes to implementing new working models (“working from home”), three-quarters (74%/2024: 81%) recognise no difference in the workload compared to their countries of origin. With 86% of mentions, the digitization of the business causes almost as much trouble for foreign fund companies in Germany as in their home market (2024: 74%).

Rules on ESG names should have little impact on existing funds

Since November last year, newly launched investment funds in Europe have to follow stricter requirements if they include terms such as “sustainable” or “environment” in their names, according to the European fund regulator ESMA. From May, this regulation will also apply to existing funds. What does this mean for the ESG range of foreign fund companies active in Germany?

According to the survey, six out of ten participants (62%) see no reason to change the names of their ESG funds as a result. Only 17% intend to do so; even fewer (14%) will adapt their investment process to comply with the new regulations. 3% stated that their company would probably merge ESG funds; the same proportion was unable to answer the question.

Nine out of ten employees are allowed to work from home more often than in the office

The most common weekly “work from home” model among the surveyed investment representatives of foreign companies is now “3 days at home / 2 days in the office” (44%), followed by “I can choose freely” (26%) and “4 days at home / 1 day in the office” (19%). “2 days at home / 3 days in the office” only applies to 7% of respondents. A full five-day presence in the office is only expected by 4%.

“How has the proportion of women working in your company changed over the past year?” was another question. For more than half of the participants (56%), the proportion has remained the same (2024: 43%). It is striking that at 26%, only half of the previous year (50%) confirmed an increase in the proportion of women.

Large institutional clients, private banks, FoF managers most important target groups

The most important target groups for the distribution of foreign investment companies in the German market are large institutional clients such as pension funds, pension schemes and insurance companies (19%), followed by fund-of-funds managers/asset managers and private banks (18% of mentions in each case). Further down the rankings were (Single) Family Offices (13%), savings banks (12%), independent financial advisors (11%) and Volks- and Raiffeisenbanken (9%).

Equities and bond funds dominate, private debt and hedge funds catch up

Equity (24 providers), bond (23) and multi-asset funds (15) remain the dominant asset classes offered by foreign fund companies since their market entry in Germany. The biggest leaps since then have been in private debt (eight providers today/three when they entered the market), hedge funds/absolute return strategies (twelve providers/six) and cash/currency products, where the number of providers has doubled from one to two.

[1] Percentage figures do not always add up to exactly 100 per cent due to subsequent rounding.